Distributed PV: primed, but not yet ready to shine

On January 2014, the National Energy Administration announced a target of 8 GW of distributed solar PV and 6 GW of utility-scale PV for 2014. Distributed PV will play an increasingly important role in China’s energy mix in the next years as part of the country’s efforts to tackle air pollution.

[caption id="attachment_3086" align="alignnone" width="1600"]

In January, China officially announced a target of eight gigawatts of distributed photovoltaic systems and six gigawatts of utilityscale installations for 2014.

In January, China officially announced a target of eight gigawatts of distributed photovoltaic systems and six gigawatts of utilityscale installations for 2014.Source:Wikipedia/Peter23[/caption]

In 2013, the Chinese PV market exploded with an annual installed capacity of 11.8 GW. Due to the national feedin tariff (FIT), around 73% of those installations were groundmounted power plants primarily built in the north and northwest provinces, far from the load centers in the east. Delayed grid connection coupled with the persistent curtailment of PV electricity from transmission line constraints has prompted the government to aggressively pursue the deployment of distributed photovoltaic (DPV) systems. In 2013, only 23% (2.7 GW) of all PV installations in China were distributed. In January 2014, the National Energy Administration (NEA) announced a target of 8 GW of DPV and 6 GW of utilityscale installations for 2014.

Setting Golden Sun, rising FIT

The previous scheme supporting the deployment of DPV was the Golden Sun Program. It ran from 2009 and concluded in June 2013 with a final capacity subsidy of 5.5 RMB/W. This program brought online around 5 GW of DPV systems but did not foster highquality installations.

Since the subsidy was capacity and not productionbased, some developers cut corners on the installation at the expense of longterm system production. Additionally, some developers committed out right fraud by installing cheaper components while claiming to have installed more expensive components. Due to the problems that arose from the capacity based subsidy under the Golden Sun Pro gram, the government instituted a productionbased feedin tariff for DPV and utilityscale systems in the reform of the national FIT on August 2013. The FIT for DPV is 0.42 RMB/kWh and, unlike the groundmounted FIT, is the same value across all of China.

Even though the national FIT for DPV does not discriminate between regions, provincial and local governments are stepping in to make their provinces and cities more attractive. Jiangsu and Shandong provinces seem to be the most promising for DPV due to their high gross domestic product, provincial FITs, large industrial base and numerous solar companies. The provincial governments across China offer a combination of productionbased and capacitybased subsidies. Jiangsu, for example, offers an additional 0.2 RMB/kWh FIT for DPV systems.

In August 2013, the central government also approved 18 DPV demonstration projects totaling 1.8 GW to be built in the industrial parks and development zones in the eastern provinces. These projects were intended to test the fea sibility of DPV systems, but none have been finished. The problems encountered reflect the wider problems plaguing the DPV industry such as a lack of financ ing, challenges with property rights and contract issues, as well as structural and electrical problems.

Despite the central government’s sup port, DPV has been slow to take off in China and may struggle to reach the 8 GW target in 2014. However, as the government adjusts its policies and the industry develops new business models, the industry will grow to play a substantial role the Chinese PV market.

[caption id="attachment_3090" align="alignnone" width="3296"]

“We are going to declare a war on our own inefficient and unsustainable model of growth and way of life,” said Chinese Premier Li Keqiang at a press conference on March 13, 2014.

“We are going to declare a war on our own inefficient and unsustainable model of growth and way of life,” said Chinese Premier Li Keqiang at a press conference on March 13, 2014.Source: Xinhau/Chen Jianli[/caption]

The DPV business model

In China, PV electricity can be consumed onsite or exported and still receive the FIT. If DPV electricity is exported to the grid, the user receives the 0.42 RMB/kWh FIT in addition to the wholesale coal fired tariff in the range of 0.4 RMB/kWh making the total price around 0.82 RMB/ kWh.

Steven Han of Solarbuzz China told pv magazine, “The levelized cost of electricity (LCOE) for DPV electricity in China, including the value added tax, is approximately 0.8 RMB/kWh, compared to the coalfired electricity costs of 0.2–0.3 RMB/kWh in the west and 0.4 – 0.5 RMB/kWh in the east of China.” With an LCOE of 0.8 RMB/kWh, exporting electricity to the grid at a price of 0.82 RMB/kWh is barely profitable.

If DPV is selfconsumed in the building, the user will receive the FIT on top of displacing retail electricity. The retail price of electricity varies across China and across different tariffs. Unlike in the USA where residential rates are higher than commercial rates, residential rates in China are substantially lower. Additionally, government buildings, hospitals, and universities in China are not considered commercial users and so have electricity rates more similar to residential customers.

Residential electricity rates average around 0.5 RMB/kWh, whereas commercial and normal industrial electricity rates are around 1 RMB/kWh. This makes commercial and industrial users the most attractive customer segment for DPV projects. The revenue stream from selfconsumption in commercial and industrial buildings could be around 1.42 RMB/kWh compared to 0.92 RMB/ kWh in residential.

In addition to a lower effective price for DPV electricity, residential DPV has other major complications. Receiving the FIT in residential buildings requires the building owner to own the rooftop. In many residential apartment buildings, each flat is individually owned. Therefore, receiving the FIT requires the developer to obtain signatures of approval from 60% of the building’s residents. Once that is finished, the contract must then specify how the benefits will be divided, which is often a more daunting challenge.

In a residential building, a DPV system could potentially provide power to multiple flat owners, but this is because the flat owners share a single electrical connection to the grid. For selfconsumption, the DPV system must be connected behind the meter. If the system’s grid connection occurs on the distribution side of the meter, the DPV system must sell electricity to the grid company. This rules out a business model where a large DPV system within an industrial park could sell electricity to multiple building owners within the park. Only if the multiple buildings use the same electrical meter could a DPV system sell electricity to multiple buildings.

Given the complications and lower price for residential DPV and the restrictions on the location of the grid connection, the most promising business model for DPV is to provide onsite power to commercial and industrial buildings.

While residential buildings are twice as prevalent as commercial and industrial buildings – 60% of all buildings in China versus only 30%, respectively – there is still great potential for DPV systems on commercial and industrial buildings. In his November 2013 China Solar PV Briefing Paper, Frank Haugwitz of the AsianEuropean Clean Energy Advisory (AECEA) stated, “Overall, according to Chinese estimates the rooftop potential in just [the industrial zones/development parks] throughout the country shall amount to approximately 80 GW.”

Given the current market trends, Steven Han told pv magazine, “While electricity prices are different in each province, generally speaking, DPV for commercial and industrial users will reach grid parity in 2017 – 2018.”

Wang Si Cheng of the Energy Research Institute (ERI) in the National Development and Reform Commission (NDRC) calculates the internal rate of return (IRR) for a selffinanced commercial and normal industrial DPV system with 80% selfconsumption to be around 17%. When the same calculation was run for a financed project, the average IRR dropped to 15%.

Despite the lower IRR, financed systems are likely more attractive to commercial and industrial users than a selffinanced DPV system because they do not have to pay 100% of the system with their own capital. Due to the higher risk of investing in China and the stronger desire to reap shortterm profits, building owners are more likely to seek out shorter term, higher return projects with paybacks around two to three years. Currently, the payback period for a DPV project in China is around six to seven years, which makes it unattractive for building owners to finance on their own.

The thirdparty financing model in China might deviate from the SolarCity model prevailing in the U.S., where the third party will receive the FIT and coalfired tariff from the grid company and sell PV electricity to the building owner at a discount to the retail rate. A different thirdparty model in China may involve a more passive thirdparty financing entity, like a bank, and another third party selling the power to the grid and/ or offtaker. As the DPV market matures, there is potential for other thirdparty financing models to develop.

Contract risk

[caption id="attachment_3088" align="alignright" width="373"]

Source: Wang Si Cheng, Intersolar 2014 Presentation[/caption]

Source: Wang Si Cheng, Intersolar 2014 Presentation[/caption]Even with a generally defined business model, there remain many challenges to developers and financiers in finding the best building owner and constructing a mutually satisfying contract.

The FIT contract in China lasts for 20 years and because the profitability of the project relies on selfconsumption, the investors need to choose a building owner who will still be in business in that time. Given the high uncertainty facing many businesses and manufacturers in China, finding such a person can be a major challenge. Even if the investor can find a building owner with a fairly secure future, the building owner may be reluctant to use PV electricity.

The DPV value proposition for building owners is a lower price of electricity and revenue from renting out their rooftop. As an example, DPV electricity may be sold at around a 10% discount to the grid price. However, the discount coupled with the rental revenue may not be enough to overcome the building owner’s uncertainty about the DPV technology.

Even though China has been manufacturing PV modules for well over a decade,

the domestic application of the technology began only a few years ago and has

mostly been concentrated in power plants in the sparsely populated northwest. DPV is unfamiliar to most building owners, so educating them on the value, safety, and reliability of solar PV is essential to get customer buyin. Industrial building owners may hesitate to incorporate this seemingly new technology into a manufacturing process for fear of having the intermittent electricity source disrupt their production.

Safety is also a legitimate concern for building owners and developers. Due to quality problems affecting PV power plants in the western provinces and weak building regulation in China, many building owners may fear the threat of a system malfunction, like an electrical fire. Developers for their part need to be careful of structural weaknesses in the roof. Many industrial rooftops are built from colored steel that is less sturdy than concrete and has a lifespan of only five to 10 years. To gain customer’s trust, developers must establish a track record of safe and reliable installations.

There is also significant contract risk in China. Even if the building owner does not go bankrupt over the contract period, he may suddenly decide he does not want to pay for PV electricity anymore. The legal system is not as efficient in China as in many developed countries, so the third party cannot simply settle the breach of contract in court. Often, this disagreement must be settled between the building owner and the third party. Perhaps the building owner is simply holding out for a lower price of electricity.

A draft report on the Chinese PV industry by MAP Royalties, a U.S. firm focusing on the management of energy royalties, underscores this point by saying, “Customers have an even stronger negotiation position after the PV is installed, since they may refuse to pay for the electricity generated from the PV system, or request removal of the PV system if a better deal comes up.” Breach of con tract presents a significant risk to DPV system developers and thus makes selecting a reliable and trustworthy building owner all the more important.

Selecting a building owner remains a major challenge, but finding interested investors is also a hurdle given the early stage of the DPV market in China.

[caption id="attachment_3089" align="alignnone" width="650"]

China has been manufacturing PV modules for well over a decade, but the domestic application of the technology began only a few years ago.

China has been manufacturing PV modules for well over a decade, but the domestic application of the technology began only a few years ago.Source: JA Solar Co. Ltd.[/caption]

Financing challenges

Like in most newly developing markets, financing is a major hurdle for DPV systems in China. Currently, the large investors in the DPV segment are equipment suppliers who are constructing projects with their own capital and hoping to sell them to utility companies, stateowned enterprises (SOEs), or building owners. Still, a major source of capital to finance projects comes from the banks, and after the Suntech and Chaori Solar bankruptcies, they have become more hesitant to lend to PV module manufacturers.

One way for manufacturers to get around debt financing from banks is by forming joint ventures. In September 2013, Trina Solar signed a frame agreement with the Hunan provincial government to develop 1 GW of DPV projects in Hunan province over the next five years. Afterward, Trina set up the wholly owned subsidiary Hunan Trina Solar to support the local market demand. Trina Solar is now in negotiations to form a joint venture with the new energy subsidiary of the China Southern Power Grid Company to develop DPV projects in southern China, a member of Trina Solar told pv magazine. The joint venture is expected to be signed by the end of the year.

Taking a different tack, Yingli Solar has formed joint ventures with energy generation SOEs. In 2014 Yingli signed two joint ventures to develop DPV projects with the China National Nuclear Cor poration (CNNC) and the Datong Coal Mine Group, the third largest coal mining SOE in China. With CNNC, it plans to develop 500 MW of distributed systems, 200 MW of which will be located at CNNC sites. The Datong joint venture did not specify a targeted capacity but follows in the footsteps of a 20 MW system built with Datong in an economic zone in Shanxi province.

DPV has proved to be too small a market for SOEs to get involved in directly. SOEs have greater access to bank financing than private companies, but they consider DPV too risky, too complicated, and too small for so little return. However, joint ventures like Trina and Yingli have signed have proven to be a more effective way for private companies to receive financing and for SOEs to reduce project development risk.

DPV is a new asset class in China with high risks and moderate returns, which makes more traditional lenders like banks wary of investing until the sector has had more time to mature. During Intersolar China 2014, a representative of Bank of China enforced this point by saying, “Banks have a very weak understanding of distributed generation. Many banks have listed distributed PV as a restricted industry.” Due to the small project sizes, banks treat DPV projects as small and medium size enterprises (SME’s), an enterprise group that is consistently overlooked by the Chinese financial system.

Big Chinese banks and SOEs would rather invest in largescale power plants because they are more familiar, simpler to construct, and have fewer involved parties. Even though the investment is larger, power plants offer higher returns.

Despite the wariness from traditional lenders, there are financing companies in China that are expanding into the DPV market. The China Financial Leasing Company (CFLC) has capital in place and a team of 45 professionals working to reach a 500 MW financing goal for 2014. While the CFLC has devoted significant resources to the 500 MW goal, Zisen Li of the CFLC seemed to have more questions than answers when speaking at Intersolar China. His main concerns included the logistics of bill collection as well as installation quality and standardization.

Project insurance is another financial tool that could be used to ease traditional lenders’ concerns over quality. AON COFCO Insurance Brokers is currently involved in creating insurance policies for utilityscale power plants but could move into the DPV segment as it grows. Having an insurance policy on the output of the DPV system has two substantial benefits to reduce the lender’s perceived risk. Firstly, the lender knows the system has been vetted and reviewed by the insurance company or a thirdparty auditor. Secondly, if the system does encounter problems, the insurance policy will provide compensation for any loss in production.

Cost remains the critical unknown for project insurance. The project developer must maintain a sufficient margin while adding on an additional insurance policy. The insurance needs to find a zone where premiums are high enough to cover the risk for the insurance company, but low enough so that the profitability of the DPV system is not compromised.

Private companies are another potential source of project finance because of the unique regulations on the Chinese banking system. The return on bank deposits in China is capped by the government, which creates greater demand for assets that can offer higher returns. Currently, private companies prefer more conventional assets like real estate, but as the DPV market develops, private companies could take a greater interest.

Like banks and SOEs, private companies would see a single DPV project as being too small to invest in. However, if DPV projects could be packaged together, in a way similar to the 500 MW agreement signed by Yingli with CNNC, they may be able to attract large investors. For example, China Development Bank does not invest in schemes under 100 million RMB, so DPV would only reach this size by pooling projects.

Finally, provincial and local governments could also step in to provide direct or indirect support by creating DPV development funds or by guaranteeing project loans. Guangdong province is currently experimenting with financing vehicles for DPV systems.

Permitting and regulation

[caption id="attachment_3093" align="alignright" width="365"]

Source: WangSiCheng of ERI/NDRC[/caption]

Source: WangSiCheng of ERI/NDRC[/caption]Permitting and regulation remain the last major challenge for DPV development. The central government has been supportive by putting policies in place to streamline the permitting process for DPV, but the follow through by the provincial and local governments has been much slower on the ground.

Just as with building owners, there is a lack of education on the part of local officials in the permitting and regulation of DPV systems. Additionally, the lack of standardized system design makes permitting more challenging.

There even seems to be some confusion on the part of developers on how to register for the FIT and receive permits for DPV systems.

To help promote distributed generation, the central government has removed grid connection charges for DPV systems. The central government ordered the two stateowned grid companies, the China Southern Power Grid Company and the State Grid Corporation of China, to allow free grid connection for DPV systems below 6 MW.

While removing the grid connection fee has helped reduce costs, there seem to be mixed views on the grid corporations’ eagerness to allow DPV systems to connect to the grid. The grid corporations only own and manage the grid and do not own any generation assets, but DPV still poses a threat to their business as it decreases the sales of electricity through the grid. Moreover, the grid corporation has no financial incentive to connect DPV systems since it is only a cost without revenue. Still, representatives from the State Grid Corporation insisted that it is supportive of DPV systems.

The MAP Royalties report reinforces this point by saying, “Although the State Grid and the Chinese government both announced progressive policies regarding distributed PV incentives on production and connection, it is still unclear at the local level how those policies can be implemented.”

Conclusion

The central government commissioned the 18 demonstration projects to test their DPV policies and because those projects have faltered, it is conducting a review of 1.8 GW worth of projects currently underway. The review should be completed in the next few months and depending on its findings, the central government may respond with further policies to support DPV if it thinks the present market problems will prevent deployment from reaching the 8 GW target.

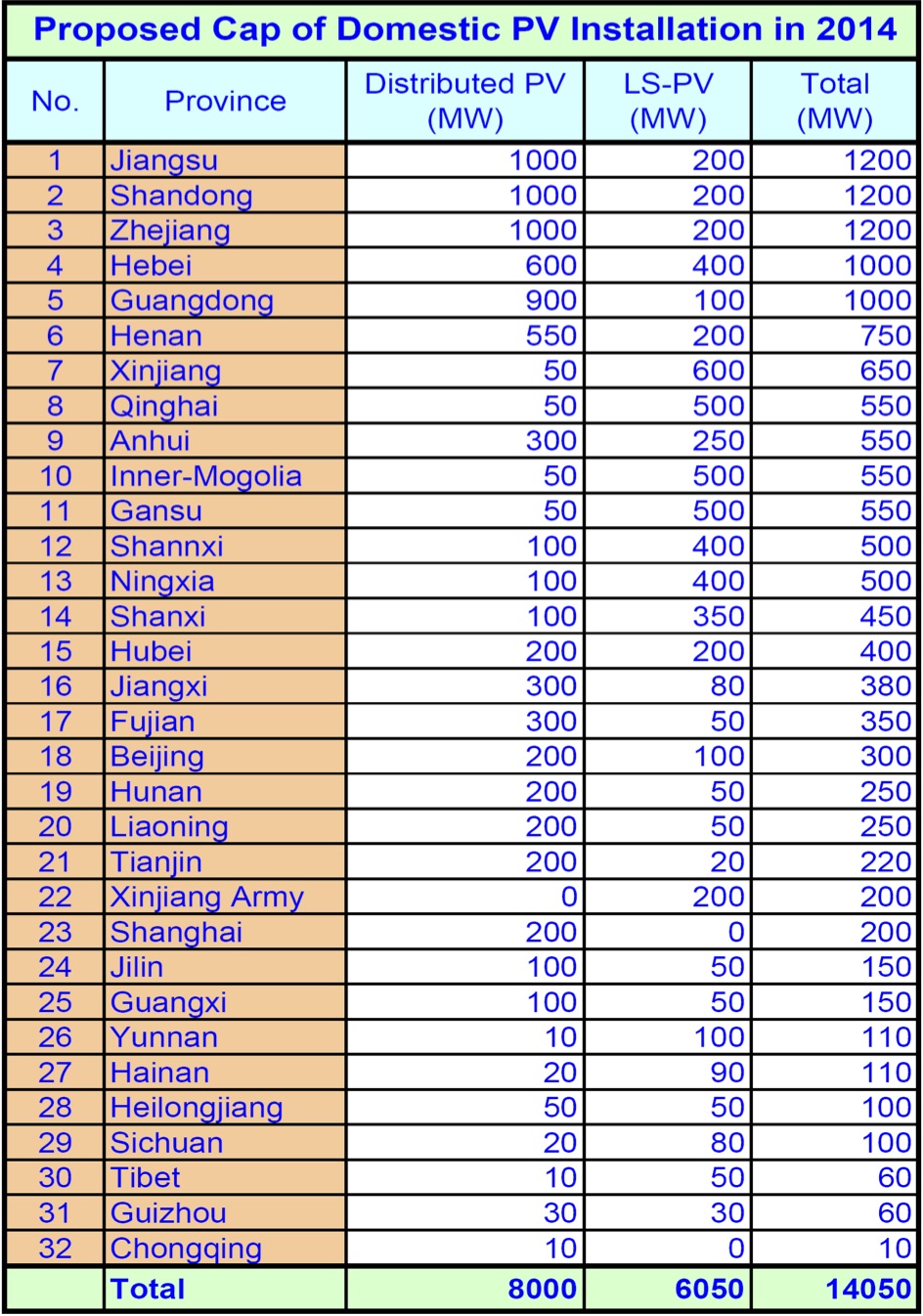

To enforce the targets, the government has released provincial caps for both distributed and utilityscale PV. The caps may serve as an effective way of diverting investment from utilityscale to DPV projects. Last year, about 8.5 GW of utilityscale projects were constructed, but only 6 GW are allowed under the caps for 2014. Utilityscale projects built beyond the 6 GW cap will not receive the FIT.

Frank Haugwitz in his January 2014 China Solar PV Briefing Paper writes, “It remains to be seen how Gansu province will scale down from approximately 3.2 GW in 2013 to just 550 MW in 2014.” While Gansu only has a small cap for DPV (50 MW), some provinces like Hebei that saw large utilityscale investment in 2013 have a high DPV cap of 600 MW. It is plausible that as developers bump up against the utility-scale caps in each province, more investment may be diverted to DPV projects. At least, that is the government’s hope.

Haugwitz continues to write in his January 2014 Briefing Paper of another government program to support DPV deployment. “In an attempt to ensure a realization of the 8 GW distributed generation projects, in early February 2014 the NEA released a list of 81 socalled New Energy Demonstration Cities, and eight socalled Industrial Demonstration Zones, spread across 28 and 8 provinces, respectively.” By 2015, the cities and zones are required to reach certain DPV capacity targets in terms of MW of DPV installed.

With all the challenges confronting the growth of the DPV industry in China, hitting the 8 GW target may seem unlikely, but the variety of government support mechanisms may be effective in overcoming these challenges. Even if the government does not meet the 14 GW annual target for 2014, it is on track to meet the 35 GW target for 2015.

Having seen PV markets overheat in response to overgenerous subsidies in Europe, the central government is being much more careful in subsidizing its domestic PV industry. While the government may not reach the 8 GW target in 2014, it seems to be more interested in building a stable DPV industry while minimizing the bill.

The National Renewable Energy Development Fund, which funds all renewable energy subsidies in China, was running a €2.5 billion deficit at the end of 2012 due to a large amount of renewable deployment in 2011 and 2012.

To plug this deficit the government has had to increase the surcharge levied on all electricity bills three times. While the deficit remains small in comparison to Spain’s electricity deficit that Reuters reported at €23.1 billion in February 2014, the Chinese government is not eager to oversubsidize their solar PV market.

While many doubt China’s ability to reach the 8 GW target, some in the industry, like Wang Si Cheng of the Energy Research Institute, remain optimistic. “I believe we still can reach the 8 GW. We are just in the first quarter of 2014 and there are many people working hard to overcome the challenges to DPV.”

Even if the 8 GW target is not reached this year, the central government seems genuinely committed to supporting the DPV industry. Not only can DPV provide an inexpensive and easily deployable energy source for a country that plans to double its generation capacity by 2020, but it can also provide a pollutionfree energy source for cities that are increasingly plagued by hazardous levels of pollution.

In a speech in March, Li Keqiang, the Premier of China, said, “We will resolutely declare war against pollution as we declared war against poverty.” DPV solar power is a critical part of the central government’s arsenal in its war on pollution. Expect to see DPV play an increasingly significant role in China’s energy mix going forward.